There are several ways that doing your taxes can actually put more money back into your pocket.

Federal tax credits are kickbacks from the government to incentivize certain behaviors or provide relief for certain expenses. Whether you’re a seasoned taxpayer looking to utilize every credit possible in your tax strategy or a newbie just dipping your toes into the world of taxes, learning about different tax credits can have a big impact on how much you owe or get back.

Let’s dive into tax credits and how they can help you save money.

Table of Contents

What is a tax credit?Are tax credits different from deductions?Who is eligible for tax credits?7 Common tax credits you should knowHow to claim tax credits?What is a tax credit?

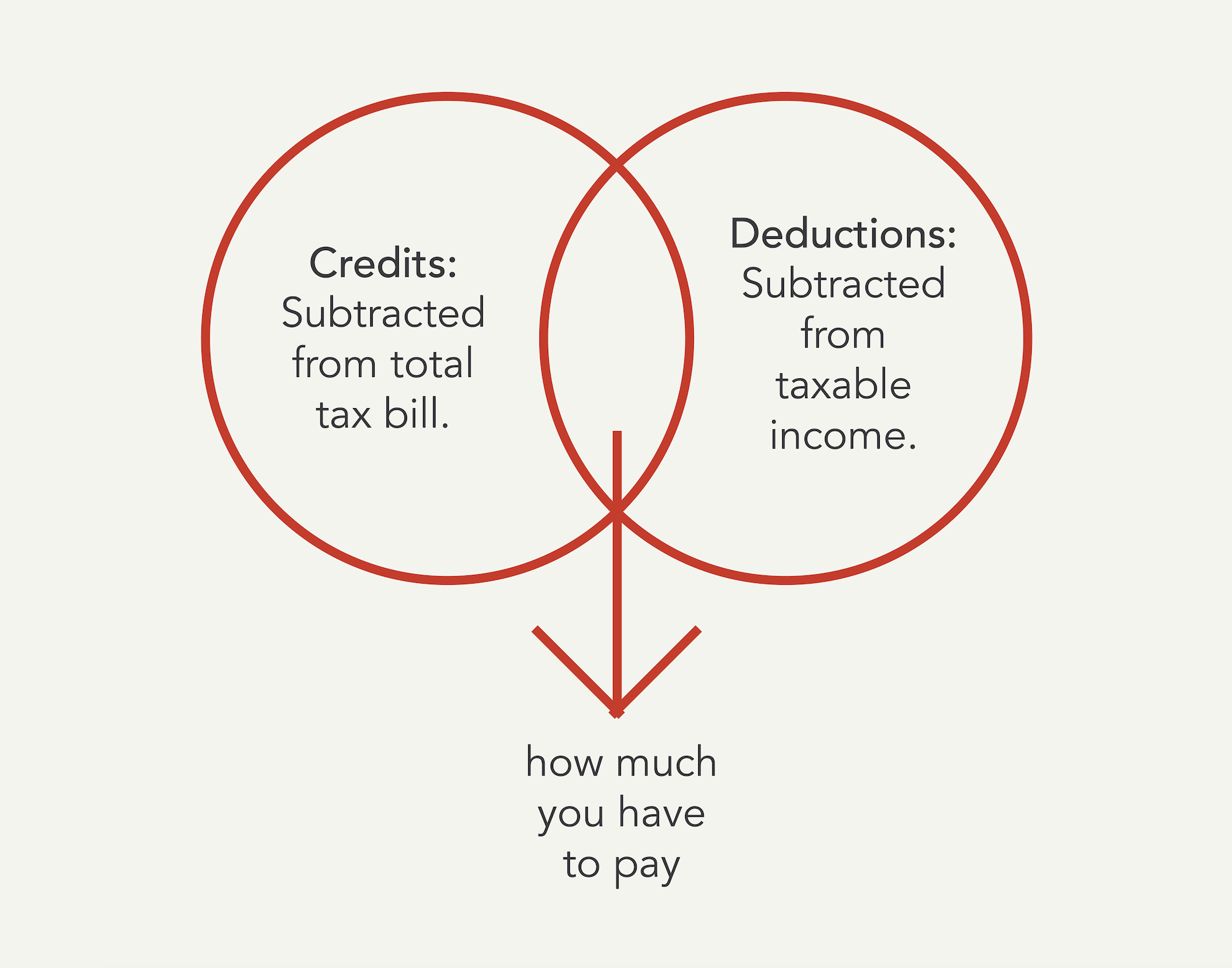

A tax credit directly reduces how much you owe. Federal tax credits help you retain your hard-earned money by reducing your tax bill dollar for dollar.

Unlike deductions, tax credits don’t reduce your amount of taxable income. Instead, they reduce the amount of tax you owe overall. The more tax credits you qualify for, the less you’ll end up owing.

So, what is a tax credit? There are a wide variety of tax credits that serve specific purposes. One tax credit example is the American Opportunity Tax Credit (AOTC), which applies to education expenses. Then, there are other tax credits for homeowners, such as the Residential Energy Efficient Property Credit. There are even tax benefits for having kids.

Basically, there are numerous tax credits that can help you lighten the load when it comes time to pay your tax bill. Whether you’re a student hitting the books, a homeowner going green, or a hardworking individual just trying to make ends meet, understanding tax credits can help you save more.

How do tax credits work?

Now that we understand what they are, how do tax credits work? Tax credits are subtracted directly from your total tax bill. This means that with each credit, you’re reducing the amount of tax you owe to the government.

Let’s look at an example. If your tax bill is $4,000 and you qualify for a $1,000 tax credit, your tax bill decreases to $3,000. Simple enough, right?

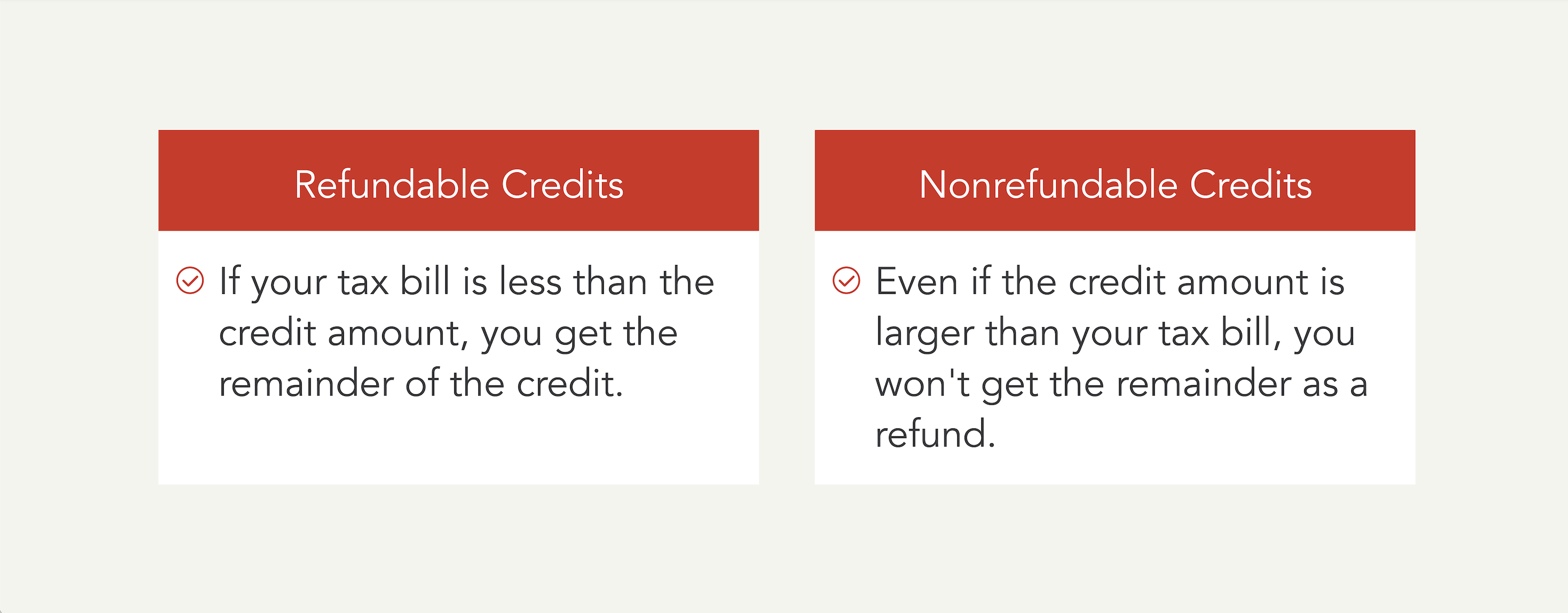

Refundable vs. nonrefundable credits

There are two main types of tax credits: refundable and nonrefundable. Refundable tax credits can result in a refund on your tax return if the credit amount exceeds how much you owe. Nonrefundable credits, however, only reduce your tax bill to zero. Even if the credit is more than you owe, you don’t get any of that leftover money.

Are tax credits different from deductions?

While both tax credits and deductions can help lower your overall tax bill, they function differently. The key differences lie in how they affect your taxable income and the amount of tax you owe.

Deductions reduce your taxable income, meaning you’re taxed on a lower amount of income. Tax credits reduce the amount of tax you owe dollar for dollar after your taxable income has been calculated.

When it comes to calculations, deductions are usually subtracted from your gross income, while tax credits are applied directly to the amount of tax you owe.

Who is eligible for tax credits?

Eligibility for tax credits varies depending on the type of tax credit. Here are some of the most common factors that can impact eligibility for various tax credits:

- Income level: Many tax credits are targeted towards individuals and families with lower to moderate incomes. There are often designated thresholds in place to determine eligibility. If you fall within or below these thresholds, you’ll typically be eligible for the credit.

- Filing status: Filing status (single, married filing jointly, married filing separately, head of household, or qualifying surviving spouse) can impact your tax credit eligibility as some credits are only available to specific filing statuses or may be applicable for different amounts.

- Dependent status: Certain tax credits require that you have qualifying dependents–children or other dependents for whom you provide care. The number and age of dependents can influence the amount of the credit you’re eligible to receive.

- Expenses incurred: Some tax credits are based on specific expenses incurred by the taxpayer. For example, you must have incurred qualified educational expenses such as tuition and fees to claim the American Opportunity Tax Credit (AOTC).

- Life events: Various life events can affect your eligibility for the credit and the amount you’re eligible to receive. Notable life events include changes in income, family size, or health insurance coverage.

Specific criteria outlined by the IRS determine if you’re eligible to receive certain tax credits. Make sure to review eligibility requirements for each credit carefully and stay up to date on tax law changes.

7 Common tax credits you should know

Are you maximizing your tax savings? Many taxpayers miss out on various credits and deductions because they don’t know about them. In this section, we’ll explore several common and sometimes missed credits and deductions that you may be eligible for. Understanding these credits could result in significant tax savings.

Earned Income Tax Credit

The Earned Income Tax Credit (EITC) is a refundable federal tax credit designed to assist low to moderate-income individuals and families. This tax credit offers a financial boost to workers earning lower wages. It helps reduce their tax burden and potentially provide a refund.

Who qualifies: Individuals and families with low- to moderate income. Note that the credit amount varies based on factors such as children, dependents, and disabilities.

Child Tax Credit

The Child Tax Credit is available to all eligible taxpayers with qualifying dependent children under 17 years old. You can get a credit per child, which directly reduces the amount of tax you owe.

Who qualifies: You can claim the Child Tax Credit for each qualifying child who has a Social Security number. Your dependent generally must have lived with you for more than half the year, be claimed as your dependent on your tax return, and be a US citizen, national, or resident alien.

Child and dependent care credit

The child and dependent care credit provides relief for those who pay for childcare or dependent care services. This tax credit helps cover a portion of the costs incurred to care for children or dependents, enabling taxpayers to continue working.

Who qualifies: Individuals or families who paid expenses for child care to enable you to work or look for work.

Education tax credits

There are two main education tax credits: the American Opportunity Tax Credit and Lifetime Learning Credit. Both aim to alleviate the financial burden of higher education expenses. These tax credits assist taxpayers with educational costs, including tuition, fees, and other related expenses.

Who qualifies: Some of the main criteria you must meet for each of these education tax credits include: you or your dependent pays qualifying education expenses for higher education, and the student is enrolled at an eligible educational institution.

Premium Tax Credit

The Premium Tax Credit helps individuals and families afford health insurance premiums through the Health Insurance Marketplace. It assists eligible taxpayers by reducing the cost of their monthly health insurance premiums to make healthcare coverage more accessible.

Who qualifies: Your household income must fall within a certain range, you cannot use the filing status of married filing separately (unless you are a victim of domestic abuse or spousal abandonment and can meet certain criteria), and you cannot be claimed as a dependent by another person. In addition, you must meet specific criteria related to health insurance.

Residential Clean Energy Tax Credit

The Residential Clean Energy Tax Credit incentivizes homeowners to make energy-efficient improvements to their homes. Taxpayers can claim this credit to receive financial assistance for eligible expenses related to upgrades such as solar panels, energy-efficient windows, and insulation.

Who qualifies: Expenses for solar, wind, and geothermal power generation, solar water heaters, fuel cells, and battery storage may qualify if they meet requirements designated on energy.gov.

EV tax credit

The EV tax credit incentivizes taxpayers to use electric vehicles. Those who purchase qualified plug-in electric vehicles are eligible for this tax credit, which helps offset the upfront cost of purchasing an electric vehicle.

Who qualifies: A tax credit of up to $7,500 is available to those who buy a new, qualified plug-in EV or fuel cell electric vehicle. It’s important to note that you must buy the car for your own use and use it primarily in the US.

To find out if you qualify for any of these credits, review the requirements and any exclusions that may apply to your situation.

How to claim tax credits?

Now that we’ve covered how tax credits work and several tax credit examples, let’s wrap it up with how to claim them.

- The first step is determining which credits you’re eligible for based on your specific circumstances. Check IRS guidelines and criteria for each credit to make sure you qualify.

- Ensure you have all necessary documentation, such as income statements, receipts, and proof of expenses. When you file your tax return, use the correct forms and schedules to report each credit accurately.

- After double-checking your entries, submit your tax return by the filing deadline and enjoy the benefits of lower taxes thanks to tax credits.