Whether you’ve taken out a home equity line of credit (HELOC) to buy your dream home, finance home improvements, or consolidate your debt, you’re likely curious if there’s a way you can leverage it for your taxes.

The Home Mortgage Interest Deduction includes interest payments incurred under a HELOC and can reduce taxable income, thus reducing the tax you owe, but only if the funds are used on things such as home renovations or improvements.

Table of Contents

What is a Home Equity Line Of Credit (HELOC)?When is HELOC interest tax deductible?Is interest on a HELOC tax deductible when used to purchase a home?How do you deduct HELOC interest on your taxes?Determine if you qualify in a few easy stepsWhat is a Home Equity Line Of Credit (HELOC)?

A HELOC is like a credit card where you borrow against the “equity” of your home. The equity is the amount of the home that you own outright.

Many buyers use a HELOC as a way to avoid paying Private Mortgage Insurance (PMI). PMI can be triggered when making a small down payment on the purchase of a home. As a general rule, any time you make a down payment that is less than 20% of the purchase price of the home, you have to pay PMI. It’s not cheap either; you can easily pay a couple hundred dollars per month, even on a moderately sized mortgage of $250,000.

To avoid this, buyers may try a first/second mortgage combination. They take a first mortgage equal to 80% of the purchase price so that PMI will not be required. The remaining 20% is provided by a combination of a second mortgage or a HELOC, and the actual amount of the down payment.

A popular combination is what is referred to as an “80-10-10”, comprised of an 80% first mortgage, a 10% HELOC, and a 10% cash down payment. The 10% HELOC is based on the 10% equity you earned when you paid the 10% down payment. This cuts the cash required in half and removes the PMI requirement.

With a HELOC, buying a house could help your taxes this year.

When is HELOC interest tax deductible?

Is HELOC interest tax deductible? Maybe. Recently, changes have been made that affect the calculation of deductible mortgage interest.

Tax years 2018-2025

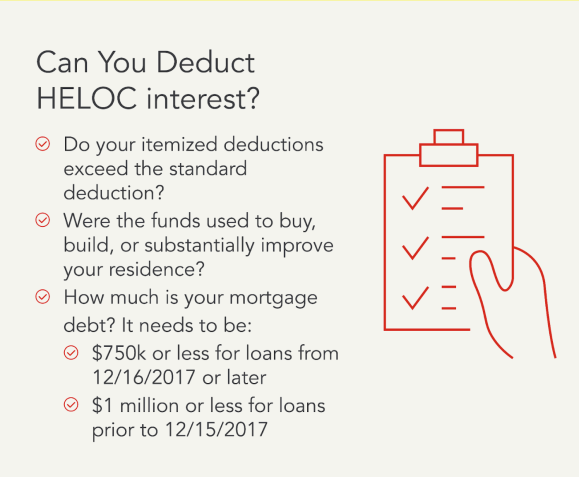

For the tax years of 2018 through 2025, home equity loan interest is tax deductible if it was secured by your main home or second home and is used to build, buy, or substantially improve the residence. Interest paid on the borrowed funds is classified as home acquisition debt and may be deductible, subject to certain dollar cost limitations.

Before tax year 2018 and after 2025

Before the tax year 2018, home equity loans or lines of credit secured by your main or second home and the interest you pay on those borrowed funds may be deductible, or subject to certain dollar limitations, regardless of what you use the loan proceeds towards. The changes that started for tax year 2018 are scheduled to expire after tax year 2025, so we might go back to the old rule.

For the years before 2018 and potentially after 2025, HELOC interest would be tax deductible even if it was used towards personal living expenses such as credit card debts.

Is interest on a HELOC tax deductible when used to purchase a home?

Fortunately, the tax considerations for interest on a HELOC used to purchase your home are virtually identical to those for your primary mortgage. As long as the HELOC is used to purchase the home, the interest will be fully deductible.

The IRS allows you to fully deduct mortgage interest paid on a total acquisition debt (mortgage balances) of up to $1 million, or only $500,000 if you are married filing separately. As long as your first-second combination mortgage arrangement is within these dollar limits, you can deduct all of the interest that you pay on both the first mortgage and on the HELOC.

With a HELOC, buying a house could help your taxes this year.

Is interest on a HELOC tax deductible when used for home improvements?

The tax-deductibility of HELOC interest is similar to when other home loans are acquired to make improvements to your home. This can include major repairs and renovations, such as replacing the roof, carpeting, or other components, such as the furnace, central air conditioner or water heater.

Interest is also fully deductible if the money is used to make major improvements. This can include renovating the kitchen and bathrooms, finishing the basement, or putting an addition on the house.

In all of the above cases, the interest that you pay on the HELOC will be fully tax-deductible. Limitations apply when money is borrowed that is not used in connection with either purchasing or improving the home, is not secured by the property, or makes your loan balances over the maximum limit.

Is HELOC interest tax deductible when used for purposes unrelated to your home?

No, not for tax years 2018 through 2025.

Starting with tax year 2026, the older rules may again apply where up to $100,000 ($50,000 if Married Filing Separately) interest paid on credit unrelated to the home may be claimed.

How do you deduct HELOC interest on your taxes?

To deduct HELOC interest on your taxes, homeowners must file itemized tax deductions during tax season using Schedule A, Form 1040, to claim itemized deductions.

Generally, a HELOC interest tax write-off is only going to be worth pursuing if all your deductible expenses total more than the standard deduction for taxpayers.

The standard deduction is a flat amount that will depend on your tax filing status.

In the 2023 tax year, for taxes due in April 2024, the standard deduction for filing status was:

- $13,850 for single filers or married couples filing separately.

- $20,800 for heads of households.

- $27,700 for married couples filing jointly.

Note that the IRS adjusts the standard deduction annually in order to compensate for the year’s inflation.

For the upcoming 2024 tax year, adjustments to the standard deduction will be applied to income tax returns due in April 2025. To elect itemized deductions for the tax year of 2024, all your deductible expenses should total over the new annual standard deduction for taxpayers, including:

- $14,600 for single filers or married couples filing separately, an increase of $750 from 2023.

- $21,900 for heads of households, an increase of $1,100 from 2023.

- $29,200 for married couples filing jointly, an increase of $1,500 from the 2023 tax year.

If you’re taking the time to itemize your deductions, don’t forget to look into other tax-deductible home improvements as you work towards investing and creating the house of your dreams.

Determine if you qualify in a few easy steps

A HELOC can provide greater flexibility in regard to either purchasing or improving your home. But if you’re going to use it for unrelated purposes, make sure you’re fully familiar with the tax benefits of doing so. If you took out a HELOC loan, TurboTax will ask you simple questions about your loan and give you the tax deduction you are eligible for.

No matter what moves you made last year, TurboTax will make them count on your taxes. Whether you want to do your taxes yourself or have a TurboTax expert file for you, we’ll make sure you get every dollar you deserve and your biggest possible refund – guaranteed.