: %

: 0%

Disclaimer: Our calculator only estimates the 24 % federal taxes withheld upfront and state taxes required to be paid. This estimate does not include your total tax you will be required to pay at tax-time based on your overall income and tax rate up to 37%.

*This calculator includes federal and state tax rates for 2024. Note for states with varying tax rates, this calculator uses the highest rate for estimation purposes.

For many people, winning the lottery is a dream come true. If you’ve ever imagined what it’d feel like to win the jackpot or what you’d do with the financial windfall, we’d bet money that you probably didn’t account for the sizable tax hit that would also come your way.

To help manage your prize money expectations, use our lottery calculator to estimate how much money goes to taxes and what you actually get to keep. Additionally, keep reading to learn more about how lottery winnings are taxed, your options for getting paid and answers to frequently asked questions.

Looking to report your latest lottery winnings on your annual tax return? Use TurboTax to accurately report your windfall.

How Much Are Lottery Winnings Taxed?

For tax purposes, the IRS considers lottery winnings to be gambling income, and under the Internal Revenue Code, they’re subject to federal income tax. In addition, lottery winnings may also be taxed at the state level, but this varies by state. Learn more about federal and state taxes on lottery winnings below.

Federal Tax on Lottery Winnings

Any lottery winnings over $5,000 have taxes withheld using the federal withholding tax rate of 24%. Depending on your prize amount, you may receive a Form W-2G Certain Gambling Winningsfrom the lottery organization telling you how much of your winnings were withheld.

You can also expect to pay taxes on these winnings because they are included in your income for the next tax season. After reporting your winnings and regular income, you may be pushed into a higher tax bracket for that year.

Reference the seven tax brackets below or use our tax bracket calculator to see exactly where you fall. The most you’ll be taxed for 2024 is 37% for any amount over $609,351 for 2024.

- Federal withholding rate for gambling income: 24%

- Federal income tax brackets for single filers in 2024:

- If income is $11,600 or less: 10%

- If income is $11,601-$47,150: 12%

- If income is $47,151-$100,525: 22%

- If income is $100,526-$191,950: 24%

- If income is $191,951-$243,725: 32%

- If income is $243,726-$609,350: 35%

- If income is $609,351 or more: 37%

State Tax on Lottery Winnings

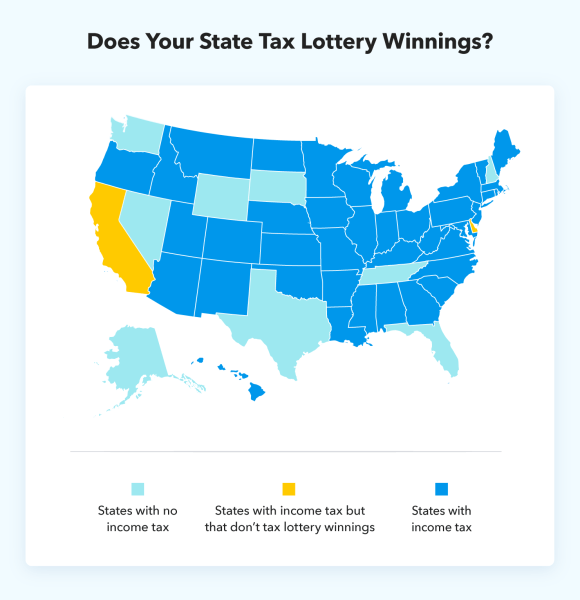

Depending on your state, your lottery winnings may also be subject to state income tax. To see the 11 states that have no income tax or don’t tax lottery winnings, check out the map below.

States with no income tax:

- Alaska*

- Florida

- Nevada*

- New Hampshire

- South Dakota

- Tennessee

- Texas

- Washington

- Wyoming

*State does not participate in lotteries such as Powerball.

States that don’t tax lottery winnings:

- California

- Delaware

It’s important to note that certain states don’t have lotteries at all, but you can always travel across state lines to buy a ticket and win big. Three out of the five states without lotteries will still tax your winnings when you report it as income on your annual tax return. These states are Alabama, Hawaii, and Utah.

Although Alaska and Nevada don’t have lotteries, if you buy a ticket in another state, you won’t pay state income taxes on any winnings. On the other hand, two other states, Arizona and Maryland, will withhold taxes on your winnings even if you don’t live there.

Whether you’re in a tax-friendly state for lottery income or not, read through the next section for how to calculate your taxes depending on which payout you choose.

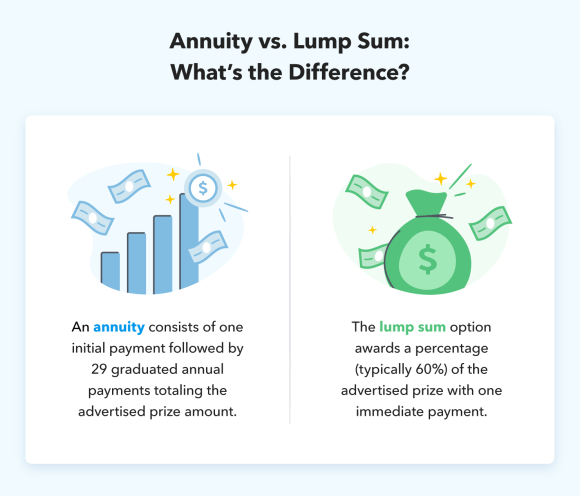

Lottery Payouts: Lump Sum vs. Annuity

When you win the lottery, you have the choice of receiving your prize as a lump sum or as an annuity. We explain how they’re different and the pros and cons of each, so you can pick the right option for you.

Lump Sum

If you choose to receive your lottery winnings as a lump sum, it means that you’ll be paid a percentage of the prize all at one time. Generally, the advertised prize amount refers to the amount paid out if you pick the annuity, and the lump sum amount is specified as a lower “cash value” or “cash option” prize.

Typically, the lump sum payout before taxes is about 60% of the advertised prize, which can help you estimate the value. As a percentage of the jackpot, you’ll receive less money than if you opt for an annuity, but taking the lump sum has its advantages (and disadvantages).

Pros:

- Gives the opportunity to invest the money and capitalize on returns more quickly

- Allows for more liquidity over funds so that you have the freedom to use them as you see fit

Cons:

- Can be challenging to manage a large financial windfall

- May lead to bankruptcy or other financial problems if spent too fast

- May triple your tax bracket

Example calculation of lump sum lottery taxes:

To put this into perspective, let’s say you live in Illinois and win a $1 million jackpot in the lottery. Learn about how you would calculate your estimated taxes and figure out the amount you keep by following the steps below.

- Step 1: Calculate the gross payout. This is typically about 60% of the lottery prize, and you’ll need to apply this to the advertised amount. You can skip this step if you know the “cash value” amount of the prize and use it as the gross payout in Steps 2 and 3.

- Gross payout = Advertised prize amount x 0.60

- Gross payout = $1,000,000 x 0.60

- Gross payout = $600,000

- Step 2: Estimate the total tax withheld. To do this, you’ll combine the federal and state tax rates and apply it to the gross payout. For this example, the federal tax rate is 24% and Illinois’s tax rate is 4.95%.

- Estimated tax withheld = Gross payout x ((federal tax rate + state tax rate) / 100)

- Estimated tax withheld = $600,000 x ((24 + 4.95) / 100)

- Estimated tax withheld = $600,000 x (28.95 / 100)

- Estimated tax withheld = $600,000 x 0.2895

- Total estimated tax withheld = $173,700 ($144,000 federal taxes + $29,700 state taxes)

- Step 3: Find your take-home winnings. You can do this by subtracting the estimated tax withheld from the gross payout, as shown below.

- Estimated take-home winnings = Gross payout – tax withheld

- Estimated take-home winnings = $600,000 – $173,700

- Estimated take-home winnings = $426,300

Annuity

Unlike the lump sum award, the annuity pays out your lottery winnings in graduated payments over time. The graduated payments eventually total the entire advertised lottery jackpot. It typically starts with an initial payment followed by graduated annual payments made over 29 years, and you’re taxed for this lottery income annually.

For example, the annuity for the Powerball jackpot starts with an initial payment, and the payment amount grows by 5% annually for 29 years. This graduated payment scheme is meant to account for inflation.

Over time you’ll receive the entire jackpot, but this may come with disadvantages depending on future tax rates and how you’d like to use your winnings. Read on to learn about the pros and cons of lottery annuities.

Pros:

- Offers the option for a steady income over a long period of time that continues to earn interest

- Defers taxes until the payouts arrive and may be a benefit if tax rates decline in the future

- Reduces the chance of squandering your funds too quickly

Cons:

- Prevents winners from accessing cash for investments or emergencies

- May result in losses if tax rates rise in the future

Example calculation of annuity lottery taxes

Because lottery jackpots are typically advertised as the annuity amount, you don’t need to estimate the gross payout. You’ll use the exact reward advertised as the jackpot. In this example, you live in the state of Illinois and bought a winning lottery ticket with a jackpot of $1 million.

- Step 1: Estimate the total tax withheld. Combine your federal and state tax rates and apply it to the prize amount. For this example, the federal tax rate is 24% and Illinois’s tax rate is 4.95%.

- Estimated tax withheld = Gross payout x ((federal tax rate + state tax rate) / 100)

- Estimated tax withheld = $1,000,000 x ((24 + 4.95) / 100)

- Estimated tax withheld = $1,000,000 x (28.95 / 100)

- Estimated tax withheld = $1,000,000 x 0.2895

- Total estimated tax withheld = $289,500 ($240,000 federal taxes + $49,500 state taxes)

- Step 2: Find your take-home winnings. You can do this by subtracting the estimated tax withheld from the prize amount.

- Estimated take-home winnings = Gross payout – tax withheld

- Estimated take-home winnings = $1,000,000 – $289,500

- Estimated take-home winnings = $710,500

Annuities come in the form of 30 graduated annual payments over the course of 29 years. Find an estimated year-by-year annuity breakdown for winning a $1 million jackpot in Illinois below.

| Annuity Year | Gross Payout | Federal Taxes | State Taxes | Net Payout |

|---|---|---|---|---|

| 1 | $15,051 | $3,612 | $745 | $10,694 |

| 2 | $15,804 | $3,793 | $782 | $11,229 |

| 3 | $16,594 | $3,983 | $821 | $11,790 |

| 4 | $17,424 | $4,182 | $862 | $12,380 |

| 5 | $18,295 | $4,391 | $906 | $12,999 |

| 6 | $19,210 | $4,610 | $951 | $13,649 |

| 7 | $20,170 | $4,841 | $998 | $14,331 |

| 8 | $21,179 | $5,083 | $1,048 | $15,048 |

| 9 | $22,238 | $5,337 | $1,101 | $15,800 |

| 10 | $23,350 | $5,604 | $1,156 | $16,590 |

| 11 | $24,517 | $5,884 | $1,213 | $17,420 |

| 12 | $25,743 | $6,178 | $1,274 | $18,290 |

| 13 | $27,030 | $6,487 | $1,338 | $19,205 |

| 14 | $28,382 | $6,812 | $1,405 | $20,165 |

| 15 | $29,801 | $7,152 | $1,475 | $21,173 |

| 16 | $31,291 | $7,510 | $1,549 | $22,232 |

| 17 | $32,855 | $7,885 | $1,626 | $23,344 |

| 18 | $34,498 | $8,280 | $1,708 | $24,511 |

| 19 | $36,223 | $8,694 | $1,793 | $25,736 |

| 20 | $38,034 | $9,128 | $1,883 | $27,023 |

| 21 | $39,936 | $9,585 | $1,977 | $28,374 |

| 22 | $41,933 | $10,064 | $2,076 | $29,793 |

| 23 | $44,029 | $10,567 | $2,179 | $31,283 |

| 24 | $46,231 | $11,095 | $2,288 | $32,847 |

| 25 | $48,542 | $11,650 | $2,403 | $34,489 |

| 26 | $50,970 | $12,233 | $2,523 | $36,214 |

| 27 | $53,518 | $12,844 | $2,649 | $38,025 |

| 28 | $56,194 | $13,487 | $2,782 | $39,926 |

| 29 | $59,004 | $14,161 | $2,921 | $41,922 |

| 30 | $61,954 | $14,869 | $3,067 | $44,018 |

| Total: | $1,000,000 | $240,000 | $49,500 | $710,500 |

FAQ About Taxes on Lottery Winnings

Still have more questions about lottery taxes? Find some answers to common questions below.

Do Lottery Winnings Count as Income?

Lottery and other gambling winnings are considered taxable income by the IRS. As such, you’ll need to report the value of your winnings as “Other Income” on your annual return using Form 1040.

Do Lottery Winnings Count as Income for Social Security?

If you win big in the lottery while collecting Social Security, your winnings won’t be counted as income that can reduce your benefits. Earning a regular income while receiving Social Security, however, may reduce your benefits.

Are Lottery Winnings Taxed Twice?

Because lottery winnings are considered taxable income, they’re subject to taxes at the state and federal levels just like regular income. Whether or not you pay state income taxes on your lottery prize depends on the state you file in.

Closing:

Winning the lottery is a life-changing event that may afford you newfound wealth and opportunities. With that being said, it’s important to be aware of how lottery winnings are taxed, so you’re not surprised by the amount of actual winnings you receive.

Use our lottery calculator to get an estimate of the taxes withheld and find out how much you’ll actually keep. Once the next tax season rolls around, use TurboTax to help you report your income as accurately as possible. Don’t forget to connect with a TurboTax Live tax expert if you have any tax questions that need answers.