If the idea of estate planning confuses or overwhelms you, you’re not alone. Many people know very little about estate planning and rarely think about it, understandably. Estate planning is one of those tasks in life that isn’t glamorous but is important to consider, especially as time goes on and we acquire more assets and wealth.

It’s common to draw a blank on the legal documents needed to create an estate plan, as well as determine if hiring a specialized attorney is necessary.

Whether you’re brand new to the idea or simply need of a refresher, we can help you unpack the estate planning basics in terms that are easy to understand.

Table of Contents

8 Steps for estate planningWhat is estate planning?

Estate planning is the process of determining who will receive your money and belongings, also known as assets when you pass or are no longer able to manage your own affairs.

One of the goals of an estate plan is also to minimize taxes so that your loved ones can get the maximum amount of any assets you choose to leave them.

Who needs an estate plan?

The word “estate” might make you think of mansions and copious amounts of money, but you don’t need to have expensive personal property and real estate to benefit from an estate plan.

If you pass without having a valid estate plan in place, the distribution of your belongings will be left up to the courts. Estate planning helps guarantee that your loved ones won’t have to go to court and face a difficult and lengthy process to get access to what you’ve left behind.

What documents will you need for estate planning?

Most estate planning begins with writing a will, which should contain all the instructions as to who will receive your assets when you pass or become incapacitated. Advance care directives like power of attorney and living wills are also often recommended when making an estate plan. Those with a certain amount of wealth might also set up a trust to hold their assets and distribute them accordingly when it’s time.

Note that these taxes are separate from estate planning (but are still helpful to know about):

- Inheritance taxes: A tax paid by the recipients of an inheritance (many states do not impose inheritance taxes)

- Gift tax: Unlike inheritance taxes, gift taxes are paid by the gifter. There is a different limit each year for how much you can give to one person before you pay taxes. For 2023, it was $17,000 per individual, and in 2024, it is $18,000.

8 Steps for estate planning

Here is a general estate plan guide where we have broken down key steps you’ll want to take to create your own estate plan.

Take Inventory of Your Assets

The first step you should take when planning your estate is to evaluate all the items, tangible or intangible, you have in your name. We’re partial to making lists, but choose whatever method best suits you.

Tangible (physical) assets can include:

- Real estate – houses, land, etc.

- Jewelry

- Family heirlooms

- Cars and other vehicles

- Furniture

- Art

- Electronics

- Antiques

Intangible (non-physical) assets can include:

- Checking and saving accounts

- Retirement accounts like 401(k) or IRA

- Health savings accounts (HSA)

- Investments like stocks and bonds

- Life insurance policies

- Patents, trademarks, copyrights

Make sure you take everything you own into account; anything you forget may be left to the courts to handle.

Assess Your Goals

This might seem obvious, but it’s a good idea to take some time to think about what is important to you when build your estate plan. It won’t be the same for everyone.

Are there specific things you want to provide for your children or loved ones? You may want to donate a portion of your estate to a certain charity. If you own a business, you might want to make sure ownership is passed on to the right person.

When you know what is most important to you, it’ll be easier to choose which estate plan is best for you.

Determine Guardianship

If you have children or pets that need to be taken care of, you’ll want to designate someone you trust to take care of them should anything happen to you. This should be included in your will. If you don’t have a will or don’t designate a legal guardian for your dependents in your will, the courts will appoint a legal guardian.

It would also be a good time to consider who you’ll name executor of your will. You’ll want this person to be someone you know and trust to handle the responsibility. Most people choose a family member to execute their will, but some prefer to choose a friend, accountant, lawyer, or financial institution.

Gather Documents

Once you know what assets you have and who you want to give it to, it’s time to get the required paperwork done. While this isn’t the most fun part of the process, it’s crucial to have the basic documents when getting your affairs in order.

Here are some of the main documents you’ll likely need while doing your estate planning:

- Will: This is where you designate the recipients of all your property and assets and assign an executor who will carry out your wishes when the time comes. If the value of all your assets is on the lower end and you don’t think you need an estate plan, you’ll still want to execute a will.

- Power of Attorney: Most estate plans include a power of attorney (POA) form that allows someone you trust to act on your behalf, which is important if you become mentally incapacitated due to an injury or illness. There are 2 types of POAs:

- Durable POA: Gives your appointed person the power to manage your financial affairs.

- Limited POA: Lays out more specific circumstances in which the appointed person would take over your financial affairs.

- Advance Healthcare Directives, which can include the following:

- Living Will: A written statement of your wishes for your own healthcare and end-of-life care should you become unable to express informed consent.

- Durable power of attorney for healthcare: You appoint someone to make healthcare and end-of-life decisions for you if you’re unable to do so.

- Trusts (if applicable): A trust gives a third party person or institution (like a bank) permission to manage money for the good of the beneficiary. The two most common types of trust are living trusts and testamentary trusts:

- Living Trust: A trust account that is formed while you’re alive, which you can make changes to (so long as it is a revocable living trust).

- Testamentary Trust: A trust written in your will to be formed after passing.

Whether working with a lawyer or financial planning service, or doing it yourself, you’ll want to look into all the above options so you can create the right estate plan for you.

Note that you may not need each one of these forms, depending on your wishes, the size of your estate, and if you have dependents, among other factors:

Make it Official

When you have all your paperwork, you’ll need to sign and notarize all the forms so that everything is finalized and legally binding.

Reassess Accordingly

If you have a child or buy a second home after setting up your will, you’ll want to update your estate plan with those details. You’ll have already done the majority of the leg work at this point, so amending your wishes should be a breeze.

Tell Your Loved Ones

As part of the estate planning process, be sure to inform those who are close to you of your wishes and intentions so that everyone is on the same page. This ensures there are no surprises for your loved ones when the time comes. You’ll also want to make sure to notify your chosen executor, if you haven’t already.

Consult a Professional

If you have an expert who helps you with family taxes, you’ll likely want to do the same when making an estate plan. It can be worthwhile to hire a specialized estate planning attorney or use an online estate planning service.

Calling in the experts can help streamline the process and make sure that things don’t fall through the cracks.

How does estate planning impact taxes?

Depending on the value of an estate and the state of residence, the estate might be subject to certain estate taxes. This is a tax that the government imposes on the estate itself. The executor of the estate is responsible for paying any necessary taxes.

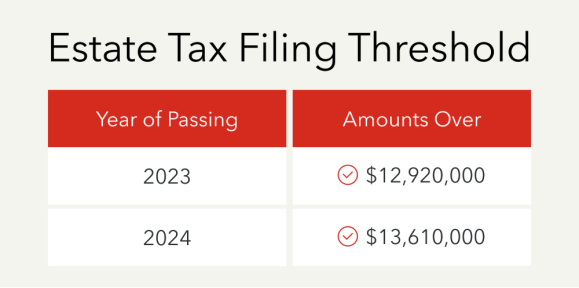

Don’t forget to look into the rules for your state of residence as well. Some states have estate taxes, some have inheritance taxes, and some have both. You might not have to pay either of these taxes depending on where you live and how much the estate or inheritance is worth. There is also a federal estate tax. Filing a return is only applicable to estates worth more than $12,920,000 for those who passed in 2023 or $13,610,000 for those who passed in 2024.