Having an IRA gives you an opportunity to save for retirement, and it has some notable tax advantages.

A traditional IRA can be a powerful tool that can help you build your savings, prepare for a better retirement, and enjoy savings when you file, like lowering your taxable income.

To help you get more acquainted with this retirement plan option, we’ll explore the key tax benefits associated with traditional IRAs, how they can enhance your savings strategy, and tips to make the most of this powerful retirement tool.

Table of Contents

Key TakeawaysWhat are the benefits of contributing to a traditional IRA?Max out your IRA contributionsMake it easy to contributeDeadline for contributing to your IRA to have it impact your taxesIf you don't qualify for the deduction, is it worth contributing to an IRA?Key Takeaways

- Contributing to a traditional IRA can reduce your taxable income.

- Traditional IRA contributions allow your money to grow tax-deferred.

- You can deduct IRA contributions.

- How much you can deduct for IRA contributions is based on your MAGI, filing status, and whether you and your spouse have a workplace savings plan.

- Qualified charitable distributions from your IRA to a charity are tax-free.

What are the benefits of contributing to a traditional IRA?

When it comes to planning for retirement and setting yourself up for a better future, it’s important to understand what you’re contributing to and what benefits you should expect down the line.

The tax benefits of an IRA are also worth considering if you’re debating between an IRA vs. 401(k), although many people may have both.

Tax-deferred growth

One of the most notable traditional IRA tax benefits is tax-deferred growth. This means you won’t pay taxes on your untaxed earnings or contributions until you’re required to start taking minimum distributions at age 73, or until you withdraw them.

This can lead to significant growth over time because the more you invest over the years, the more you’ll have to withdraw when you hit retirement age, considered to be 59 ½.

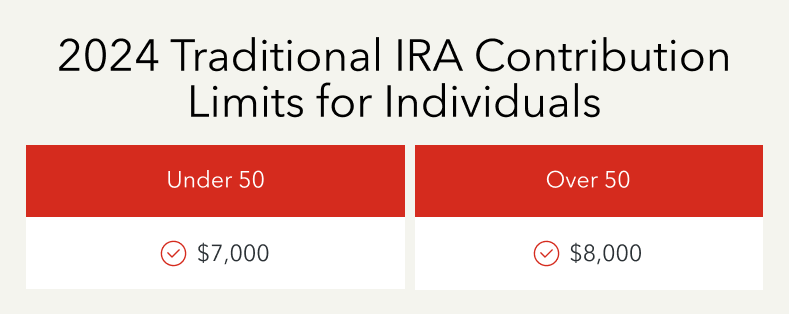

It’s important to note that there are contribution limits for a traditional IRA. In 2024, the contribution limit is $7,000 for individuals under 50 and $8,000 for individuals 50 or older. These limits include the total contributions you make for contributing to a Roth IRA and your traditional IRA.

Tax-deductible contributions

Another traditional IRA tax benefit is the deduction for contributing in the first place. Whether you can deduct your contribution is based on your modified adjusted gross income (MAGI) and the access you and your spouse (if you have one) have to an employer plan such as a 401(k).

If neither you nor your spouse are eligible for a workplace savings plan, then you may be eligible to deduct the full contribution amount, no matter what your income is.

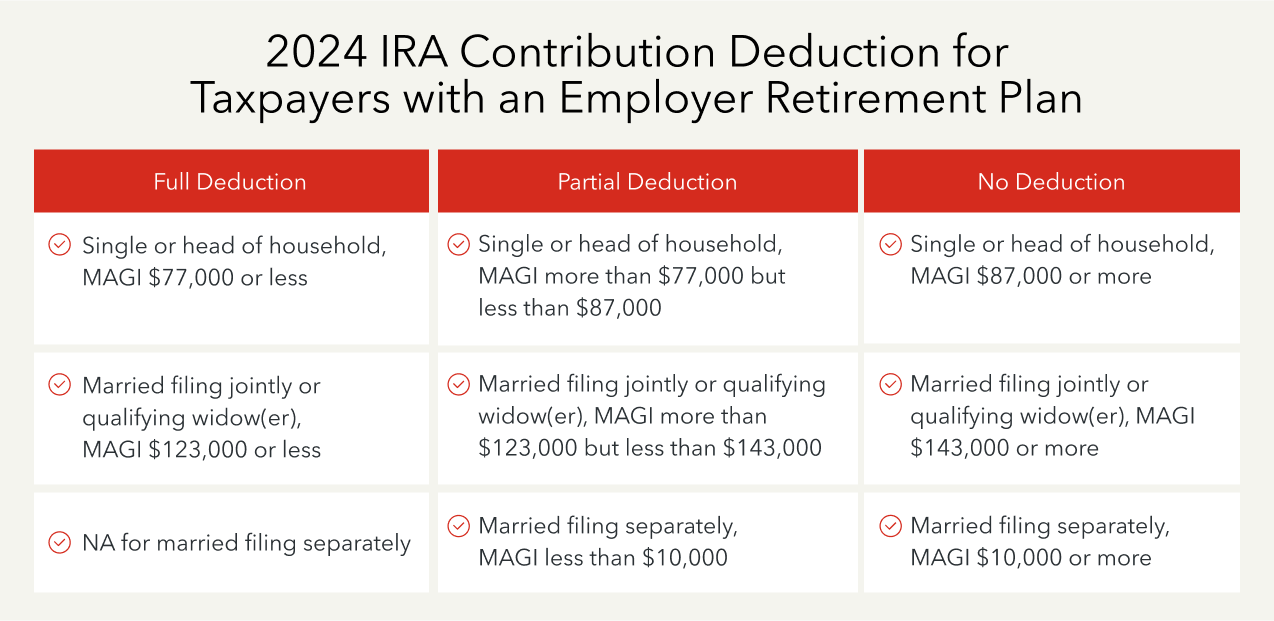

If one of you is eligible for an employer retirement plan, then deductibility is phased out at higher incomes. For 2024, the following rules apply:

- If you’re filing single or head of household, and your MAGI was $77,000 or less, you’ll receive a full deduction up to your contribution (within the limits for traditional IRAs).

- If you’re filing single or head of household, and your MAGI was over $77,000 but less than $87,000, you’ll receive a partial deduction.

- If you’re filing single or head of household, and your MAGI was $87,000 or more, you won’t receive a deduction.

- If you’re married filing separately, and your MAGI was less than $10,000, you’ll receive a partial deduction.

- If you’re married filing separately, and your MAGI was $10,000 or more, you won’t receive a deduction.

- If you’re married filing jointly or as a qualifying widow(er), and your MAGI was $123,000 or less, you’ll receive a full deduction up to your contribution (within the limits for traditional IRAs).

- If you’re married filing jointly or as a qualifying widow(er), and your MAGI was more than $123,000 but less than $143,000, you’ll receive a partial deduction.

- If you’re married filing jointly or as a qualifying widow(er), and your MAGI was $143,000 or more, you won’t receive a deduction.

So, if you or your spouse are covered by an employer retirement plan, you can still make contributions to a traditional IRA, but depending on your income, contributions may only qualify as partially tax-deductible or totally non-tax-deductible IRA contributions.

No matter how much you can deduct, the other tax benefits of traditional IRAs are worth considering when determining whether this savings plan option is right for you.

Qualified charitable distributions (QCDs)

A qualified charitable distribution (QCD) is a tax-free donation from an IRA to a qualified charity. If you are 70 ½ or older, you’re eligible to make QCDs directly from your IRA to the qualified charity of your choice.

With certain requirements, QCDs can count towards your required minimum distributions (RMDs) for the year and aren’t included in your taxable income..

When donating to an IRA, especially through qualified charitable distributions, distributions must be made directly from your IRA to an eligible 501c3 charitable organization. An individual can donate in a calendar year, across all charities, up to $105,000. If you are married filing taxes jointly, your spouse can also donate up to $105,000 from their IRA as well. With a QCD distributions are not treated like taxable income and helps offset the chances of being pushed into a higher tax bracket.

Max out your IRA contributions

When should you start investing in an IRA? As soon as you can, provided that you have an emergency fund in place and don’t have any high–interest (>12%) debts.

How much can you contribute to your IRA? For 2024, the total contributions you can make to your IRA is $7,000 or $8,000 if you’re age 50 or older. If you’re married, you can contribute a total combined amount of $14,000 (under 50) or $16,000 (over 50). If you can max out your contributions, it may be worthwhile.

With IRA contributions, there are guidelines for the deduction and contribution limits. If you contribute to your traditional IRA by April 15, you may be able to claim a tax deduction on your tax return for the amount contributed. Roth IRA contributions, however, are not tax deductible since the qualified distributions are tax-free.

Don’t worry about figuring out these limitations. TurboTax easily guides you through the necessary entries and gives you the appropriate tax deduction to maximize your tax refund.

Make it easy to contribute

The easiest way to stay on target for your investment goals is to go ahead and automate your IRA contributions. It can be as small as $25 per week; the important part is getting you into the habit of saving up for your retirement.

You can also set aside a chunk of any bonuses or windfalls you get this year to deposit into your IRA.

Deadline for contributing to your IRA to have it impact your taxes

Tax day, April 15, is the day of your tax return filing deadline, (not including extensions), and is also the deadline to make contributions to your traditional or Roth IRA and have the contribution impact your taxes. Just make sure that your financial institution knows which year you are applying the contribution to.

If you don’t qualify for the deduction, is it worth contributing to an IRA?

If you don’t qualify for tax deductions, it’s easy to get discouraged about contributing to an IRA, but that doesn’t mean it’s not worth it.

Contributing to an IRA is an easy and tax-free way to give your money a chance to grow and save up additional dollars for retirement. Plus, the earlier you start contributing, the more opportunity you have for your wealth to build.

With a traditional IRA, you can defer, but not escape, federal taxes on that income. But, since your income will most likely be lower when you’re retired–if that’s when you withdraw–you’ll likely fall within a lower income tax rate, meaning you’ll pay less on that income you put away than you would now.

Keep in mind IRA withdrawal rules, too. If you need to withdraw money before age 59 ½, you may be hit with a 10% penalty fee unless you qualify for an exception.