Tax loss harvesting is one potential strategy you can use as an investor to not only help you reduce your taxes but to increase your portfolio as well. While this is a common tax strategy used by investors, it is not suitable for all situations. This article will cover the things you will need to know before you get started.

Table of Contents

What is tax loss harvesting?How does tax loss harvesting work?What types of investments does tax loss harvesting work on?Navigating tax loss harvesting rules & regulationsTax Harvesting: The StepsIs tax loss harvesting worth it?What is tax loss harvesting?

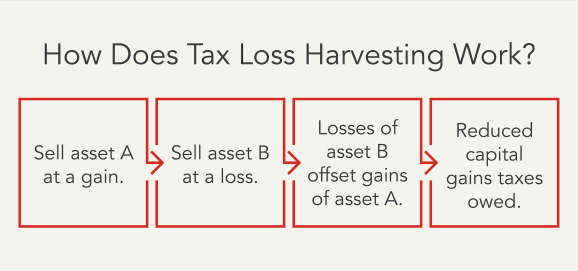

Tax loss harvesting is when you sell (otherwise known as “harvest”) investments at a loss to offset or reduce the capital gains tax that you owe. Tax loss harvesting may be a strategy that’s worth considering if you have an investment that is losing value.

For example, you may have a long-term investment that you’ve lost money on over a few years and a couple of investments that you will realize gains on once you sell. Since you’re losing money on one of your investments, it may be best to sell it and take the capital loss. This will reduce the amount of capital gains taxes you owe on the investments that did well, leaving you with more money to reinvest and grow your portfolio.

While tax loss harvesting can be an effective strategy for some investors, it’s not right for everyone. Before using this strategy, it’s important to understand how it affects your tax return and your investment portfolio.

How does tax loss harvesting work?

When you make money from an investment — otherwise known as a capital gain — you often have to pay taxes on the profit. Taxes on stocks and other investments are called capital gains taxes. Capital gains taxes can add up quickly, and have a big impact on your taxes due so tax loss harvesting can be an attractive option if you’re looking for ways to save. It’s important to understand that there are different types of capital gains taxes — long-term and short-term. If you hold an investment for more than a year before selling it for a profit, it is considered a long-term capital gain. If you sell an investment that you have held for less than a year, it is considered a short-term capital gains.

One of the most important things to understand is the difference between short-term and long-term capital gains. If you sell an investment before holding it for a year, you make short-term capital gains or losses. These are taxed at a higher tax rate – your income tax rate – which is 0% through 37%, depending on your taxable income.

If you hold an investment for more than a year, it’s considered a long-term investment. These are taxed at the lower long-term capital gains rate, which is 0% through 20%, depending on your taxable income.

With tax loss harvesting, your capital losses are first used to offset capital gains of the same type. The remainder will be used to offset the remaining gains, whether they’re long or short term.

If you don’t have any capital gains to offset or your capital losses exceed your capital gains, you may be able to use up to $3,000 ($1,500 if filing married filing separately) to offset your regular taxable income. There is no time limit on the number of years you can carry over your loss. However, if you are not going to experience frequent large capital gains or have other income to offset, then accumulating such losses may not be beneficial to you.

What types of investments does tax loss harvesting work on?

If you’re considering tax loss harvesting, it’s important to understand the different types of investments and the role they play in your portfolio. Tax loss harvesting only works on taxable investments, including stocks, mutual funds, securities, and other types of investments. Tax-free investments like 401(k)s, municipal bonds, IRAs, 529 plans, and HSAs can’t be used for tax loss harvesting.

You can even use tax loss harvesting on crypto. This is when you sell crypto at a loss to offset any capital gains you may have had during the year. As with any typical tax loss harvesting strategy, the amount you “harvest” in any particular year will depend on the income you want to offset.

Navigating tax loss harvesting rules & regulations

Although tax loss harvesting seems relatively simple, there are some additional rules and regulations to consider.

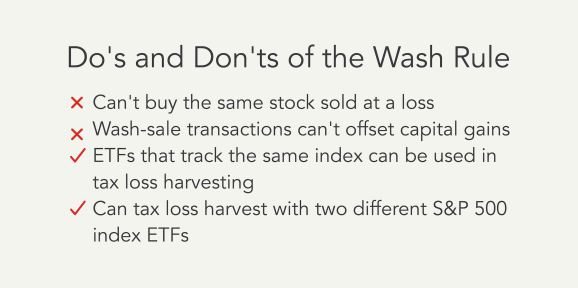

The wash sale rule is one of the biggest factors to consider. A wash sale is when you sell an investment at a loss and then purchase the same investment or something very similar (or as the IRS calls it – “substantially identical”) within 60 days. This 60 days consist of 30 days before and 30 days after the sale of the investment. Since many investors want to use their tax savings to increase their portfolio, they must take the necessary precautions to ensure they do not violate the wash sale rules, or else their loss may be disallowed.

Keep in mind that wash sale rules take into account any account that is made under your social security number (and your spouse’s, if applicable). Therefore, even if stock is sold in a brokerage account and repurchased in an IRA account, wash sales rules would be violated, and any loss would be disallowed.

Tax Harvesting: The Steps

Before you start investing, you should understand how tax loss harvesting works and how you can use it to your advantage. Tax loss harvesting can be a useful strategy for investors, but you need to know how your decisions impact your taxes and portfolio. If you make a mistake, you may not be able to use your capital losses to offset your capital gains.

Here’s a simple breakdown of the steps:

- Start by selling your unprofitable investment at a loss. Before you do so, make sure this investment can be used for tax loss harvesting, and you are not violating any wash sale rules.

- Use the capital losses from your unprofitable investment to offset capital gains derived from other parts of your portfolio. If you don’t have capital gains, you can offset up to $3,000 ($1,500 per person if for Married Filing Separately) in regular income using tax loss harvesting.

- Replace your unprofitable investment with another investment that’s not too similar to keep your portfolio diverse and to avoid wash sale violations.

Is tax loss harvesting worth it?

Tax loss harvesting is not for everyone. While it may offer a benefit for investors in all tax brackets, tax savings will be greater in higher tax brackets. In addition, you must have the right kind of securities and make sure you won’t violate wash sale rules.

Whether you’re just getting started or you’re an experienced investor, you may be able to take advantage of your capital losses to save on taxes. If you’re not tax loss harvesting, don’t worry. No matter what moves you made last year, TurboTax will make them count on your taxes. Whether you want to do your taxes yourself or have a TurboTax expert file for you, we’ll make sure you get every dollar you deserve and your biggest possible refund – guaranteed.